50, 150, and 300 – Number of civilian nuclear power plants under construction, on order, and planned, respectively, which according to the World Nuclear Association are going to be looking for long-term Uranium contracts these coming decades.

The bulk of these reactors are in the Asian region, and it’s expected, barring a major breakthrough in renewables, that Africa will get in on the action in due course of time.

Back in May, 2007 I wrote about an interesting conversation I had with a speaker who was a proponent of the Climate Change theory, and a self-confessed disciple of Al Gore’s ‘An Inconvenient Truth’. Even back then it was evident that nuclear power would play a huge part in any conversation about carbon neutral power. Yes, that’s right I was high on Uranium back then, as I’m now.

Then came the Fukushima disaster, and most companies dealing with, mining for, and working with Uranium saw their stock plummet, I mean share prices crashed and burned, even marquis companies like Cameco lost 80% of their value, as for smaller and less well-known companies? In some cases like Skyharbour Resources, Denison Mines et al. prices went down as much as 90 to 97 percent.

Now however, nuclear power has started gaining traction once more, you have to keep in mind after the initial hysteria, the people in charge realized that despite the disaster there was not one provable case where anyone was affected by radiation, and that the Fukushima disaster hit a 1970s reactor without the loss of a single life contributable to radiation.

As the world’s thirst for cheap green energy grows nuclear power in general and uranium related investments will slowly but surely start attracting interest, and that’s because even some of the doyens of the green movement are grudgingly coming around to the notion that Carbon is the immediate Global threat, and nuclear fuel is the surest way to achieve any measurable progress to keep rising temperatures down to less than the 2° C as agreed to in the Paris Climate Conference.

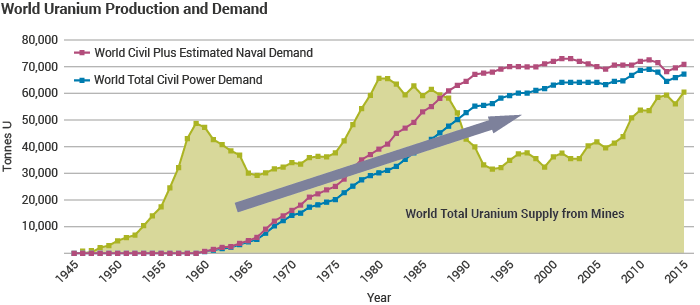

Which brings us back to the future of Uranium demand and production. Today the bulk of the world’s Uranium production (59,531 Tons of Uranium) accounts for 92% of the world’s demand, with the rest being met by existing stockpiles. This demand is poised to increase by over 30% by 2030.

Apart from Canada and Australia, a lot of the countries producing Uranium ore have interests inimical to that of the West (Uranium One anyone), and as more and more of these plants come into operation, there will be a need to secure long-term contracts to ensure a steady supply of ore, and when I say long-term I’m talking of 60+ years – which is the minimum time most new plants are designed to be active for.

Now this is the part I’m interested in, one of the reason stocks for most Uranium mining and exploration companies fell was due to a fall in world-wide prices of uranium. For some suppliers of Uranium to US nuclear power plants, it was cheaper to purchase it from abroad than mine it in the US.

Now thanks to an increase in demand and a positive political climate we can expect some of these companies who have explored and proven or are in the process of proving the economic feasibility of projects like the Dewey Burdrock, Athabasca Basin, East Preston etc. to start seeing some positive returns.

As I mentioned earlier some of these prospective companies saw hits as much as 90 to 97 percent on their share prices. They have nowhere left to go but up, and while it may take time to get there, there is very little downside set against potentially high rewards.

Along with the demand in Uranium you will see an uptick in trace minerals, rare earths, graphite, and silver – pretty much everything used in industry.

———-

Thank you for reading my post. I regularly write about private market opportunities and trends. If you would like to read my regular posts feel free to also connect on LinkedIn, Twitter or via Atlanta Capital Group Investment Management.

Greg Silberman is the Chief Investment Officer of ACG Investment Management LLC (“ACGIM”). ACGIM specializes in creating custom private market solutions for RIA/Family Office clients.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The views and strategies described may not be suitable for all investors. It is not possible to directly invest in an index. An index fund is a type of mutual fund with a portfolio constructed to match or track the components of an index. Past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. Advisory Services offered through ACG Investment Management, LLC. ACG Investment Management is an affiliate of ACG Wealth Inc.

Image: https://pixabay.com/en/atom-electron-neutron-nuclear-power-1222516/

http://www.world-nuclear.org/information-library/facts-and-figures/uranium-production-figures.aspx