2 Reasons Why the Odds are Stacked Against the Fed

We continue to hew to our favorite scenario of a market downturn in the intermediate future …

In 2 Painstaking Reasons the Market can expect a Midlife Crisis we show how total business sales have been dipping lower while total inventory build is stagnant or moving higher.

That’s a recipe for a recession!

Think about how apparel stores cope with a similar situation.

They DRAMATICALLY discount prices to move stock.

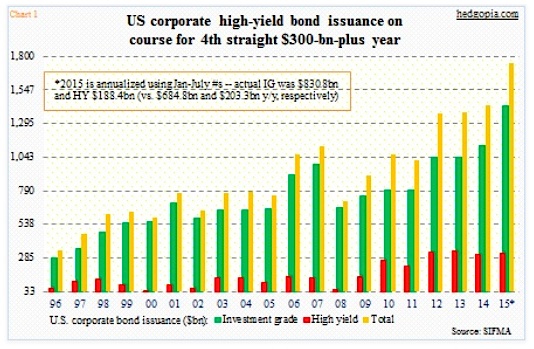

On the capital market shelf, as it were, where can we find an over-abundance of inventory?

The corporate and junk bond markets come to mind as crowded trades given recent levels of issuance:

Corporations have used this debt to:

- Buy back stock

- Make acquisitions

- Fund operations.

But wait!

9 out of 10 S&P sectors have lower consensus estimates today than January 1st.

The S&P 500 estimated earnings for Q1/16 have been slashed from $29 down to $26 during Q1/16. GDP estimates have been slashed too.

A recession would accelerate the pressure on corporate profits and leave many companies financially strapped which would surely impact corporate credit.

Revisiting our forecast for Higher Rates in 2H16.

While credit risk is becoming problematic, interest rate risk is still one of our major concerns. In our 2016 Market Forecast we said:

“Growth in the US. continues to accelerate albeit at sluggish levels by historical standards. As we approach full employment, wages begin to increase stoking (highly suppressed) inflation fears and driving long-term rates higher. “

So far we remain alone in our prediction. While employment and wage growth remain sluggish, core CPI numbers continue to come in above expectations stoking suppressed inflation fears.

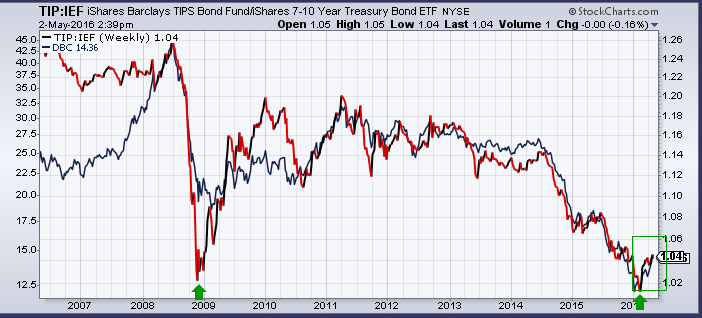

We consider the nascent trend of TIPs outperforming Treasuries (red below) as one to watch.

Someone out there is buying inflation protection!

The correlation between inflation expectations (TIPS v Treasuries) seems to visually correlate with higher commodity prices (blue line).

So what’s driving commodities higher from depressed values?

- Bearish psychology has become so overwhelming that there is nobody left to sell;

- Bargain hunting;

- Out of control money printing (China) and negative interest rates (Japan and Europe) driving money into hard assets as a store of value;

- Geopolitical tensions causing a renewed arms race – is the market discounting a war mongering President circa. November 2016?

We’re not sure but considering the facts we feel there is ample arguments to be made that support a continuation in higher commodity prices … and thus higher inflation expectations!

There seems to be a lot of risk out there, both in credit and rates, which is perhaps why the leading equity averages have gone NOWHERE in over 17 months!

The Fed is seemingly in a Catch-22;

- higher rates impact the corporate bond market negatively;

- but standing still as inflation expectations ratchet higher is not a plausible course of action either.

Stay Safe!

GREG

—

Thank you for reading my post. I regularly write about private market opportunities and trends. If you would like to read my regular posts feel free to also connect on LinkedIn, Twitter or via Atlanta Capital Group.

Greg Silberman is the Chief Investment Officer of Atlanta Capital Group. Atlanta Capital Group specializes in creating custom private market solutions for RIA/Family Office clients and is an active acquirer of independent wealth management practices.

Advisory Services offered through Atlanta Capital Group.

Securities offered through Triad Advisors, Member FINRA / SIPC.

Atlanta Capital Group is not affiliated with Triad Advisors

Nothing in this article should be interpreted as a recommendation to buy any security. Please conduct your own due diligence.

Main pic: https://raumrot.com/portfolio/set-13-free-for-commercial-use-photos/